We believe that fees should be clear, transparent, and aligned with the value you receive.

Financial planning is not just about transactions—it is about ongoing advice, structured thinking, and helping you make better decisions over time.

A Long-Term Approach

At Ifamax Wealth Management, we provide ongoing advice.

There is no initial charge for the work we do—we only charge for the ongoing service we provide.

This means we work with you over the long term, offering continuous support rather than one-off recommendations.

Our service typically includes:

Regular review meetings

Ongoing access to advice and guidance

Investment oversight and rebalancing

Retirement planning and income strategy

Tax-efficient planning considerations

This structure ensures your financial plan remains relevant as your circumstances evolve.

What You Are Paying For

While fees are often associated with visible services such as meetings or reports, much of the value comes from the work that happens in the background.

Your annual fee provides access to structured, proactive support, including:

Regular review meetings

Ensuring your plan remains aligned with your goalsOngoing financial planning

Supporting decisions as your life and circumstances evolveCashflow modelling

Helping you understand how decisions today affect your futureInvestment oversight

Ensuring your portfolio remains aligned with your risk profile and objectivesTax planning support

Making efficient use of available allowancesOngoing access to advice

You can contact us at any time—not just at review points

The aim is not just to manage investments, but to help you make confident, informed financial decisions.

Beyond Investments: Where Value Is Often Created

It is easy to focus on investment performance.

In reality, much of the long-term value of financial planning comes from decisions, not markets.

This includes:

Avoiding unnecessary tax

Structuring withdrawals sustainably in retirement

Making informed decisions during periods of uncertainty

Staying invested during market volatility

Adjusting plans as life changes

These are not always visible in a single number, but they are often where the greatest value is created.

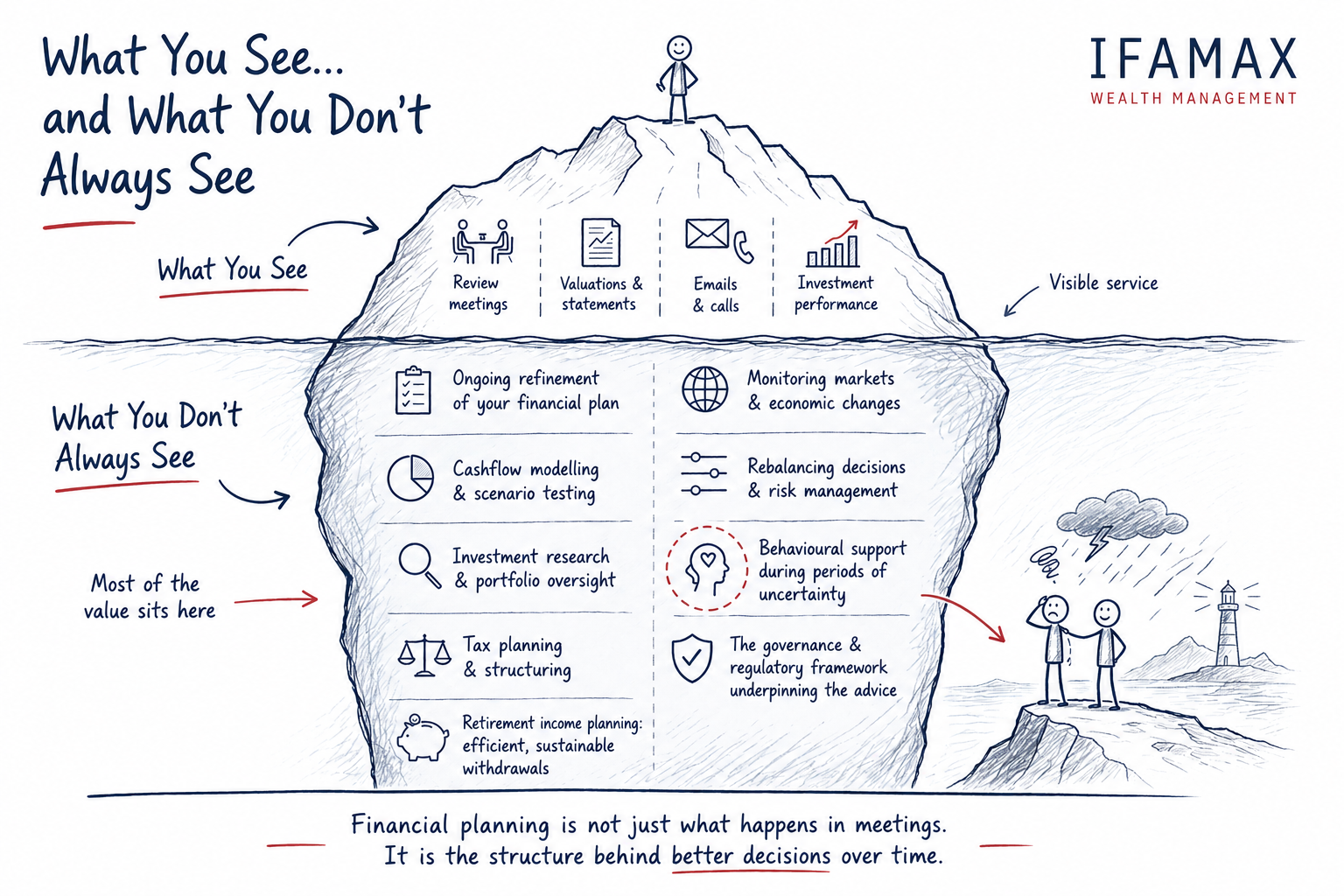

What You See… and What You Don’t Always See

When working with a financial planner, some parts of the relationship are visible and easy to recognise.

You will see:

Review meetings

Valuations and statements

Emails and calls

Investment performance

These are important and form part of the ongoing service.

However, much of the value in financial planning sits beneath the surface

What you don’t always see is the work that supports better decisions over time:

The ongoing refinement of your financial plan

Cashflow modelling and scenario testing

Investment research and portfolio oversight

Tax planning and structuring

Monitoring markets and economic changes

Rebalancing decisions and risk management

Behavioural support during periods of uncertainty

The governance and regulatory framework underpinning the advice

This work is continuous and often happens quietly in the background.

It may not always be visible in a single moment, but over time, it plays a significant role in helping you stay on track and make informed decisions.

Financial planning is not just about what happens in meetings—it is about the structure, thinking, and discipline that underpin them.

Transparency & Clarity

We are committed to ensuring that:

You understand what you are paying

You understand what you receive

There is a clear alignment between cost and value

Full details of our fee structure will be explained during our initial conversations, so you can decide whether our service is right for you.

Aligned with You

Because we work on an ongoing basis, our relationship is built on alignment.

Our focus is on delivering value over time—supporting you through different stages of life and helping you navigate financial decisions with clarity.

If You Value Ongoing Advice

If you are looking for a financial planner in Bristol who offers a structured, long-term approach to financial planning and wealth management, we would be happy to have an initial conversation.

Frequently Asked Questions

-

We believe the greatest value comes from ongoing advice rather than a single point in time.

By not charging an initial fee, we focus on building a long-term relationship in which we are aligned with you over time. We believe this is a fairer and more transparent way to work.

-

Clients often tell us they value:

Feeling more confident about retirement

Understanding their long-term financial position

Knowing their wealth is structured efficiently

Having someone to sense-check important decisions

The reassurance that their plan adapts as life changes

-

For some, managing finances independently may feel appropriate.

However, many clients value having a structured plan, ongoing support, and a trusted adviser to guide decisions—particularly as financial situations become more complex.

The value often comes from clarity, confidence, and the avoidance of costly mistakes over time.

-

We take a structured approach to monitoring the quality and effectiveness of the advice we provide.

As part of this, we carry out regular internal reviews aligned with the Financial Conduct Authority’s Consumer Duty. These are designed to identify any areas that could pose a risk to client outcomes.

This includes looking at areas such as:

Client engagement and ongoing service delivery

Financial vulnerability and changing circumstances

Retirement income sustainability

Client feedback and overall experience

Much of this work happens behind the scenes, but it plays an important role in ensuring that the advice you receive remains appropriate, consistent, and focused on your long-term objectives.

It is part of our commitment to making sure you continue to receive value—at every stage of your financial journey.

-

Yes.

While our aim is to build a long-term relationship, you are free to leave at any time. We believe this flexibility is important and reflects the ongoing value of the service we provide.

-

Fair question. Our fee buys more than a portfolio. It buys you time back, protects you from costly mistakes, and gives you the confidence of a plan that has been properly thought through. For most clients, the real value is simply never having to worry about it alone.