Inflation Never Retires — So Why Do Most Retirement Plans Ignore It?

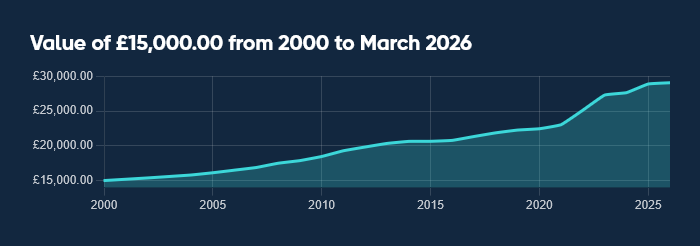

Imagine retiring in the year 2000 with an income of £15,000 per year.

At the time, that may have felt comfortable.

The average UK house price was around £86,000. Rent was significantly lower than it is today. Energy bills were a fraction of current levels, and a weekly food shop looked very different.

Fast forward to today, and that same income tells a very different story.

Using the Bank of England inflation calculator, £15,000 in 2000 would need to be closer to £29,000 today just to maintain similar purchasing power.

And in reality, many people would argue it needs to be even more.

Because retirement today comes with costs that barely existed 20 years ago:

Streaming subscriptions

Mobile contracts

Rising council tax

Higher energy costs

More travel and lifestyle spending

Which brings us to a simple truth:

Retirement is not just about building wealth.

It is about ensuring your income retains its meaning.

Section 1: Inflation Is the Silent Tax

Inflation rarely arrives with drama.

It doesn’t usually make us panic overnight.

Instead, it quietly reduces what our money can buy over time.

And in retirement, that can be one of the biggest risks of all.

Many people focus on what they need on day one of retirement.

Far fewer think about what they may need:

10 years later

20 years later

Or even 30 years later

As people live longer, inflation becomes a serious planning issue—not just an economic headline.

A retirement lasting 25 years could easily see spending power cut dramatically if income does not adapt.

Section 2: The Retirement Challenge Has Changed

Retirement planning today looks very different from that of previous generations.

Final salary pensions with built-in inflation protection are less common.

More people now rely on:

Personal pensions

ISAs

Investment portfolios

Property wealth

That means the responsibility often sits with the individual.

And retirement is no longer just about generating income.

It is about balancing:

Longevity risk

Inflation risk

Tax efficiency

Investment risk

Behavioural decision-making

This is one reason why retirement advice often attracts so much discussion around fees.

Because the challenge is rarely choosing a product.

The challenge is building an income that lasts.

3. How We Help Protect Against Inflation

At Ifamax Wealth Management in Bristol, we believe retirement planning is not a one-off event.

It is an ongoing journey.

A meaningful retirement plan should consider:

Your spending today

Your lifestyle goals tomorrow

The impact of inflation over time

How markets may affect your assets

How income may need to adapt as life changes

That is why we use:

Cashflow modelling

Scenario testing

Tax-efficient income planning

Regular reviews

Behavioural coaching during uncertain markets

Because protecting retirement income is not simply about finding yield.

It is about building resilience.

4. Retirement Is Not One Number

One of the most common questions we hear is:

“How much do I need to retire?”

It is a good question.

But perhaps not the best one.

A better question may be:

“How do I make my retirement income sustainable and adaptable as life changes?”

Because retirement is not one number.

It is a journey.

And that journey may include:

Helping children or grandchildren

Unexpected healthcare costs

Travel dreams

Lifestyle changes

Market downturns

Changing tax rules

The real goal is not certainty.

The real goal is flexibility.

Frequently Asked Questions About Inflation and Retirement

How does inflation affect retirement income?

Inflation reduces the purchasing power of your money over time. This means the same income may buy significantly less in 10–20 years.

Should retirement portfolios still include growth assets?

In many cases, yes. Retirement can last decades, so some exposure to growth assets such as Equities may help combat inflation.

How often should retirement income be reviewed?

Most retirement plans should be reviewed regularly—particularly when markets, tax rules or personal circumstances change.

Can cash alone protect me in retirement?

Cash can help with short-term spending needs, but over the long term inflation can erode its real value

H2: Closing Thought

At Ifamax, we have started a 12-month retirement education series because we believe retirement deserves more than product conversations.

We know that:

Markets move.

Inflation rises and falls.

Tax rules change.

But a thoughtful plan gives you something more valuable than certainty.

It gives you options.

Related Links

The Twelve Steps to Retirement

How Much Do I Need for a Comfortable Retirement in the UK?

Retirement Planning in the UK: How to Build a Sustainable Income for Life

When Can I Afford to Retire? How We Help You Find Your Freedom Date

Important note

This article is distributed for educational purposes only and should not be considered investment advice or an offer of any security for sale. This article contains the opinions of the author but not necessarily the Firm and does not represent a recommendation of any particular security, strategy, or investment product. Reference to specific products is made only to help make educational points and does not constitute any form or recommendation or advice. Information contained herein has been obtained from sources believed to be reliable but is not guaranteed.

Article Written: May 2026, Tax Rates and Allowances May Change In The Future.